Carbon Removal's Wrong Turn

How Market Design Created Today's Scaling Crisis

Last week's article on why we won't achieve gigatonne carbon removal sparked a flood of responses from across the industry. The resonance was clear: our current approach simply isn't designed to reach the scale we need. This overwhelming response highlighted the need for a deeper examination—to understand how we got into this predicament and, more importantly, how we can course-correct.

Having worked in carbon removal since 2015, I've witnessed the evolution of this industry from the early days when it was little more than a concept discussed by small groups around the world to today's landscape of 500+ startups and billions in investment. This isn't just a history lesson; understanding how specific market design choices created today's scaling barriers is essential for building better systems.

The Legacy Systems Problem: Carbon Removal's Offset DNA

Carbon removal didn't emerge in a vacuum—it inherited structural DNA from the existing carbon offset market, and this legacy created fundamental limitations from the start.

By 2015-2016, the voluntary carbon market was dominated by registries like Verra and Gold Standard. These nonprofit entities had established themselves as the gatekeepers of carbon offsets, but their business model created immediate barriers to scale: they charged the supply side. Developing a carbon project meant paying significant fees to get certified—often requiring custom methodologies that could take years and hundreds of thousands of dollars to develop.

The entire system was built around carbon avoidance (reducing emissions that would have occurred otherwise), not carbon removal. This introduced complex counterfactual requirements: how do you prove something would have happened in an alternate reality? For forestry projects, this meant demonstrating that forests would have been cut down without payment—leading to notorious "leakage" problems where timber operations simply moved elsewhere.

These structural issues affected every new entrant to the carbon removal space. Many early-stage companies found themselves trying to retrofit carbon removal into frameworks designed for avoidance—applying rules that fundamentally didn't make sense for this different activity. The push to eliminate counterfactuals for removal activities faced resistance from established players who saw them as essential components of "quality."

The Great Bifurcation (2020): When Permanence Trumped Scale

When carbon removal started gaining traction in 2018, a strong consensus existed around nature-based solutions. The prevailing wisdom was: "Why spend enormous resources on expensive, energy-intensive engineered solutions when natural carbon sinks like soils and forests can do the job more affordably right now and with co-benefits?"

This made perfect sense: start with the most practical, scalable approaches while developing longer-term technological solutions. But everything changed in 2020.

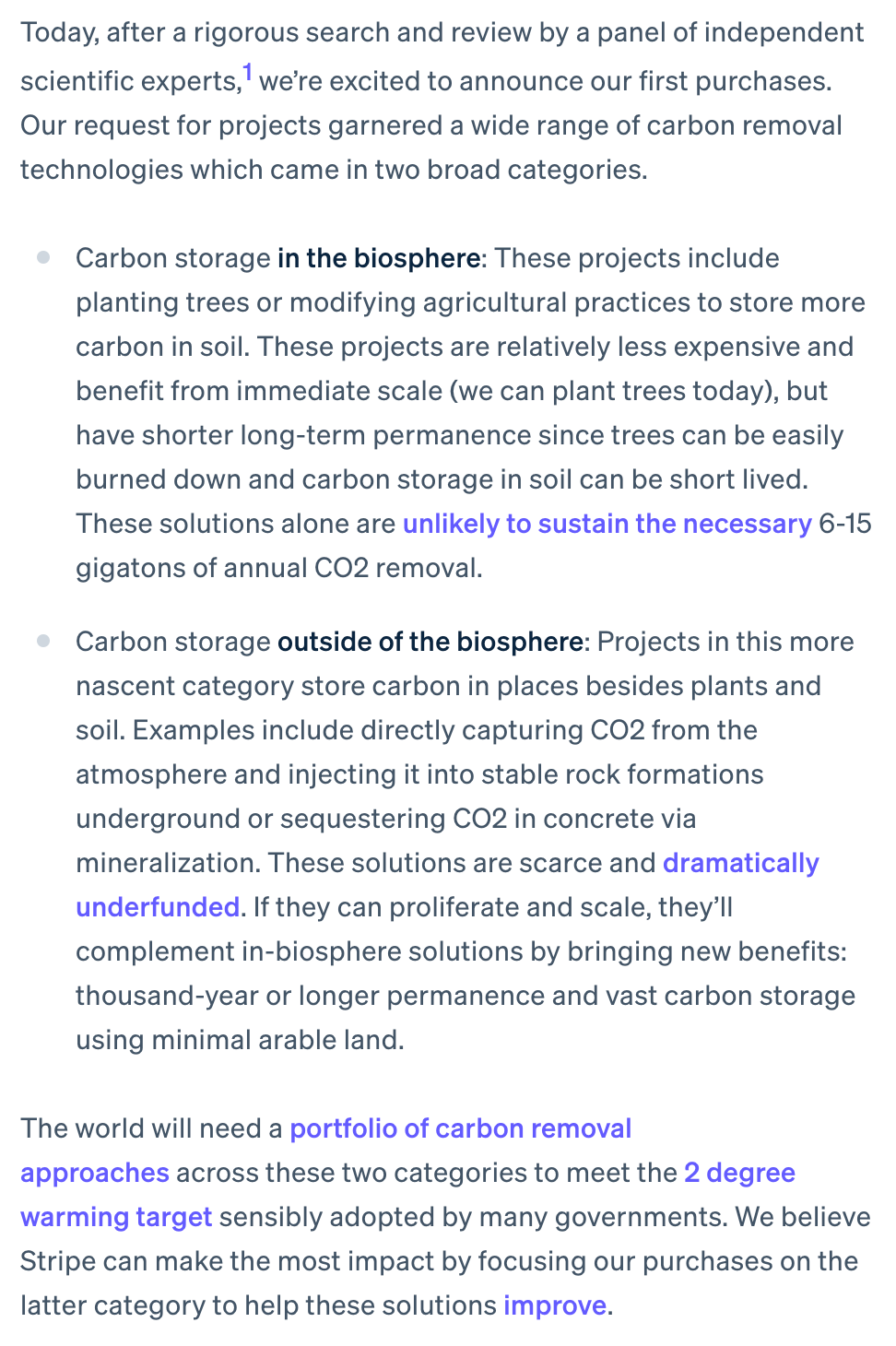

Stripe's climate commitment represented a watershed moment for carbon removal. Their initiative deserves significant credit for catalyzing corporate interest and helping educate the market about the crucial distinction between carbon avoidance and carbon removal. As the first major tech company to invest in this space, they assembled an advisory board of scientists and consultants to evaluate RFP submissions. What fundamentally altered the market trajectory was their advisory board's decision to prioritize "permanence" over scale.

The 2020 Stripe RFP received submissions from across the carbon removal spectrum. While their selections heavily favored technological approaches promising thousand-year storage, this emphasis on permanence—though scientifically defensible—had significant consequences for the industry's scaling potential. Long-duration storage solutions were at an earlier stage of development with higher costs and greater technical barriers to scale.

Shopify and Microsoft soon followed with major carbon removal commitments of their own. While both companies have invested significantly in nature-based solutions alongside technological approaches, they've directed their largest investments toward permanent removal methods.

Eventually, the Frontier Climate advance market commitment group formalized this permanence-focused approach as the de facto market standard. The result was a bifurcated landscape with drastically different price points and scaling potentials:

Traditional avoidance offsets: $3-5/tonne

Soil carbon and forestry credits: $15-25/tonne

Engineered permanent solutions: $100s-1000s/tonne

This market structure—while successful in driving innovation in long-duration carbon storage—has created a significant challenge for scaling. The industry has effectively had to choose between theoretical perfect permanence and practical near-term scale, when what we need for climate impact is both working in parallel.

The Precision Paradox: When Measurement Killed Scalability

With permanence established as the primary criteria, measurement precision became the next scaling barrier.

Corporate sustainability directors consistently express one overwhelming concern: reputational risk. As JetBlue’s sustainability director put it to me in 2017, "My biggest fear is having a reporter walk into my office saying the carbon project we funded turned out to be fraudulent."

This fear of negative press drives corporate buyers to look for "signals” that what they're buying is real and credible. They need "cover" to demonstrate that their investments are legitimate. Precision in measurement becomes one of those crucial signals—regardless of whether it's actually necessary for atmospheric impact.

If you're a layperson evaluating two soil carbon approaches, one using direct soil sample testing and another using modeling (even if that modeling is based on generalized sample testing and includes conservative discounts), you're likely to assume the direct sampling approach is inherently "better" or more reliable. This creates a market bias toward approaches that seem more rigorous to non-technical buyers, even when those approaches may be fundamentally less scalable.

This signal-seeking behavior created an impossible economic equation for nature-based carbon removal. Soil sampling can cost $50 per sample, with multiple samples needed per field. For a 1,000-acre farm potentially generating just 0.5-1 tonnes of carbon removal per acre annually, the economics simply don't work.

Yet this measurement bias largely ignores a fundamental reality: all carbon accounting involves some level of uncertainty. Even direct physical measurements contain error bars. The precision paradox created a classic catch-22: measurement approaches that provide sufficient "signal" to satisfy corporate buyers are too expensive to implement at scale, while approaches affordable enough to scale can't provide the reputational "cover" buyers seek.

This paradox isn't limited to soil carbon. Enhanced weathering, ocean alkalinity enhancement, and other promising approaches all face similar challenges—their potential scale is effectively capped by verification requirements that prioritize the appearance of precision over practical impact.

The Financial Additionality Trap

Perhaps the most restrictive legacy concept from the offset world was "financial additionality"—the requirement that projects wouldn't happen without carbon credit revenue. For carbon avoidance, this made theoretical sense: buyers only wanted to fund emissions reductions that wouldn't have occurred otherwise.

But when applied to carbon removal, financial additionality created an impossible situation. Standards bodies like ICROA and ICVCM enshrined additionality as a core principle, requiring removal projects to demonstrate they wouldn't be financially viable without credit revenue.

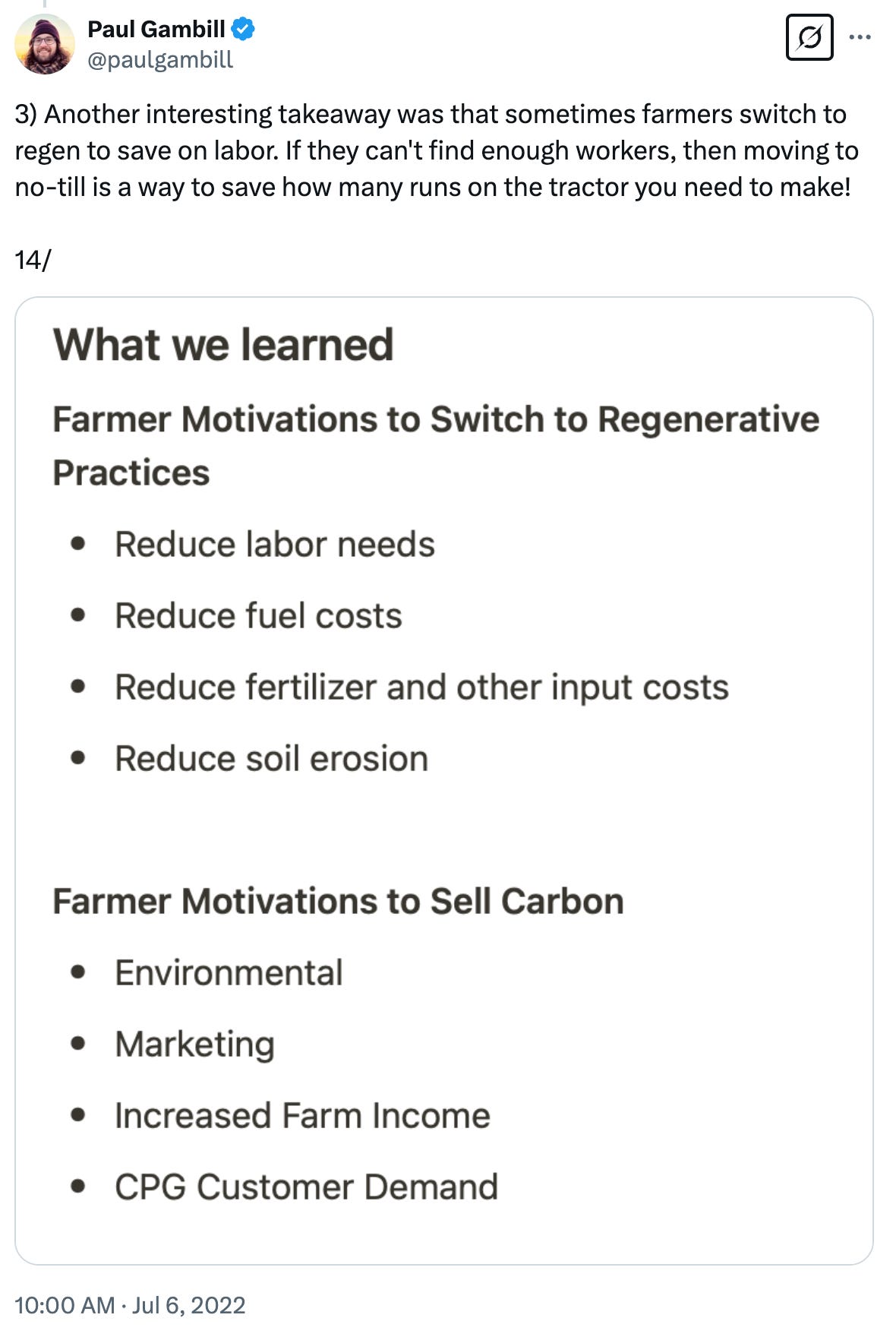

For soil carbon, this created a structural barrier to scale. The reality is that farmers don't adopt regenerative practices solely for carbon credits—they have multiple motivations including soil health, yield stability, and input cost reduction. Carbon credit revenue ($15-20/tonne) simply isn't enough on its own to drive wholesale practice change; it would need to exceed $100/tonne.

But at $100+/tonne, corporate buyers would choose other options. So the industry faced another market design paradox: prices too high for buyers but too low for suppliers, with additionality requirements preventing creative solutions to bridge this gap.

The additionality trap extends beyond soil carbon. Under strict interpretation, any removal approach that becomes commercially viable would no longer qualify as "additional." This creates the perverse incentive to maintain dependency on carbon credit revenue rather than developing sustainable business models—the opposite of what we should want for a scaling industry.

The Wrong Department Problem: CSOs vs. CFOs vs. CMOs

As the carbon removal market matured, a fundamental misalignment in market positioning became clear: the industry was selling to Chief Sustainability Officers when scale might require engaging Chief Financial Officers or Chief Marketing Officers.

Sustainability departments operate with limited budgets and narrowly defined mandates. Their primary concerns are meeting specific corporate commitments while minimizing reputational risk. This creates a fundamentally different buying dynamic than if carbon removal were positioned as a revenue driver (CMO territory) or operational concern (CFO territory).

When sustainability departments purchase carbon removal, they must justify every tonne against alternatives. They need extensive documentation, maximum certainty, and minimal risk. Their constrained budgets create strong price sensitivity, yet their risk aversion pushes them toward the most expensive, verified options. This contradiction further limits scaling potential.

What if carbon removal were instead positioned as a marketing opportunity, funded through advertising budgets? Or as infrastructure investment? Consider the rideshare example: a sponsor pays for carbon removal after your ride, giving you a carbon-negative trip, the sponsor targeted advertising, and the platform a differentiating feature—all without directly charging the sustainability department's limited budget.

This departmental mismatch affects the entire industry. Companies building carbon removal solutions repeatedly find themselves pitching to sustainability teams with limited purchasing power, when their technologies might be better positioned as marketing assets, product differentiators, or infrastructure investments.

Recent market developments highlight this concern. Several major corporations have scaled back or eliminated their carbon offsetting programs, often citing lack of ROI or shifting corporate priorities. When carbon removal is confined to the sustainability department, it remains vulnerable to changing corporate winds rather than becoming embedded in core business operations.

Breaking the Gordian Knot: Alternative Market Designs

The scaling crisis in carbon removal isn't the result of any single factor—it stems from the cumulative effect of market design choices that prioritized accounting precision over atmospheric impact. Breaking free requires fundamental restructuring, not incremental adjustment.

Three key principles should guide this redesign:

1. Separate emissions reduction from historical carbon removal

We need distinct systems with different incentives, metrics, and funding mechanisms. Emissions reduction should be driven by regulations and efficiency improvements, with carbon removal focused entirely on drawing down atmospheric carbon regardless of who emitted it.

2. Create value-generating (not just cost-generating) models

Instead of treating carbon removal as purely an expense, we need models that generate additional value. This could include:

Product integrations that create premium offerings

Advertising-supported removal (the sponsor-paid model)

Loyalty programs that incorporate removal

Cause-based marketing approaches

3. Design explicitly for scale from the beginning

New market structures must be evaluated primarily on their scaling potential. This means:

Accepting reasonable uncertainty in measurement

Embracing portfolio approaches to permanence

Creating accessible on-ramps for suppliers

Eliminating structural barriers like additionality requirements

Several companies have attempted innovations along these lines. The concept of "blended tonnes" we developed at Nori aims to balance immediate action with long-term impact by combining shorter-term removal with guaranteed future delivery of more permanent approaches. Others have explored renewal models for shorter-term storage, or infrastructure investments to reduce supplier costs. But the gravitational pull of the existing market design has proven remarkably strong.

The harsh reality is that current carbon removal systems—from registries to standards bodies to procurement practices—are structurally incapable of achieving gigatonne scale. They were designed for a different purpose: creating high-precision, fully-verified offset accounting for a relatively small number of corporate buyers.

Moving Forward: Redesigning for Atmospheric Impact

Understanding these historical design choices isn't about assigning blame—it's about recognizing that different design choices could lead to dramatically different outcomes. Everyone involved has been operating according to their own incentives and with good intentions.

But if we're serious about removing 10 billion tonnes annually by 2050, we need market structures specifically designed for this purpose:

Atmospheric impact systems that prioritize emission reduction over accounting precision

Inclusive standards that enable multiple removal approaches based on scale potential

Creative funding mechanisms beyond the sustainability department

Metrics aligned with actual climate goals rather than corporate reporting requirements

The carbon removal industry stands at a crossroads. We can continue optimizing for accounting precision and theoretical permanence within existing frameworks—and fail to reach meaningful scale. Or we can redesign the market around atmospheric impact—creating fundamentally different approaches that might not satisfy current accounting requirements but could actually deliver the scale our climate needs.

The encouraging response to last week's article suggests the industry is ready for this conversation. Now we need to translate recognition into redesign—creating market structures that align financial incentives with climate impact.

Carbon removal isn't failing because of technology limitations, insufficient funding, or lack of commitment. It's failing because we've designed systems that structurally cannot scale. Changing those systems is entirely within our power.

Excellent article!!! You hit all the right points.

I gave a talk in ... 2009, explaining why additionality, in particular financial additionality, should not be applied to a carbon removal solution such as biochar. Given the paltry amount of money available from carbon credits, the requirement that a carbon removal project would not occur without carbon credit revenue is just insane. As an example, our large scale biochar production plant costs USD 3.5 million for the kiln alone, probably closer to 4.2 million + with land, building, utilities installed, and peripheral equipment. It costs 1.8 million a year to operate. At $100 a ton CO2e, annual revenue from carbon credits would be about 650k at full production capacity, which might take years to build up to. If that carbon credit revenue would be the difference between a profitable venture and bankruptcy, nobody would ever invest in such a project.

Investors are shopping around for the best opportunities they can find, and that means they want to minimize risk and maximize profit. If they have to rely on the voluntary carbon market and its current price points just to keep from losing all the money they have put into a project, forget it. The chance to find one investor willing to take on this risk is very low, I've talked to to many of them to believe otherwise. Finding 10's of thousands of them to scale our project meaningfully while relying on carbon credits to make the difference is completely divorced from reality.

We designed our technology to scale without any need for carbon revenue. Rather it relies on a co-product, pyroligneous acid, which is a potent biostimulant and also helps build soil carbon. So it is in your value-generating category. What we still need to get this off the ground is funding that is willing to shoulder the risk of developing new markets for products that remove and sequester carbon, rather than emit carbon to the atmosphere.

Hi Paul, this article resonates with my experience and frustration with using carbon markets to assist investment in projects to reduce gigatons of emissions.

You call out the collection of norms, adopted by umpires in the field, that have an insubstantial relationship with common sense. Its recommendations, with another from your piece with Nick van Osdol, could forcefully achieve success by defanging the sillier barriers. Notably, the silliest must be additionality, set up to reward inability and punish capability.

My path to climate impact is based on a scientific and engineering discovery of deep-water-based carbon emissions reduction solutions. This family of solutions is developed, tested, and designed for scaled-up risk mitigation. It can pay its way. The IP is already proven in a Great Lake. It's now in Series-A funding, and raising funds needs carbon credits to drive the attractiveness and pace of investment.

Other far less effective, less productive solutions were built with poor technology and design, failing to earn even operating profits. Political/financial support got them on their way but never helped them develop a capable solution that could claim credits.

By contrast, after decades of R&D, we can spend $3 Billion on staged capex over a decade, achieving 7x the energy output, and potentially earning hundreds of billions from energy sales and carbon credits. Our core aim is to fully de-risk the lake's threat of gas eruption, and power up two countries. We can replace charcoal with biogas as the cooking fuel for millions of homes.

The solution is novel, both in the environment that one can operate, and in the IP through which gigatons of methane and CO2 gas can be removed, used, or safely stored for millennia. While millions of gigatons of such gases are present in the oceans and lakes, we first focus on those at risk of slow or sudden, but inevitable emissions.

With a better mindset, and less ill-informed bureaucratic control, scale-up and success can happen.